With the higher unemployment rates and increasing cost of living, it is easy to fall into debt. While you might have been confident in your ability to repay your loan when applying for it, sometimes you encounter financial hardship, which leaves you struggling.

Should You Pay A Debt Collection Agency Like LVNV Funding?

LVNV Funding, LLC is a debt collection company that purchases charged-off loans. Once they purchase a debt, they aggressively pursue the debt holder to collect it. The endless calls and numerous letters from LVNV Funding can be irritating, annoying, and scary, but they are mostly harassment. Here is how you can stop LVNV Funding.

What is LVNV Funding LLC?

Have you received a call from LVNV Funding LLC, and are you unfamiliar with the name? You might be confused about who they are and why they are contacting you.

LVNV Funding LLC is a debt collection company owned by Sherman Acquisitions that buys off charged accounts from lending companies like personal loan lenders and credit card issuers. Therefore, if they contact you, it’s for a debt you probably owe to another creditor. They mostly buy debts from Wells Fargo, Capital One, Citibank, and Chase. Their company is based in Nevada, although they pursue debtors nationwide.

A charged-off debt is when the original lender gave up collection efforts after the debtor failed to meet their payments. For example, when you take a personal loan from company A and fail to repay it, they will try to reach out and collect the debt. If their efforts to make you repay the debt are unfruitful, they might decide to charge you.

Note that a charged-off debt is not a forgiven debt. Therefore, when a lender charges off or writes off a debt, it does not mean you don’t have to repay it. The creditor might decide to sell the debt. In this case, the company, usually a debt collection agency that buys the debt, will continue to pursue you to repay the debt. So, if your debt was charged-off, and LVNV Funding LLC bought it, you will owe them the debt.

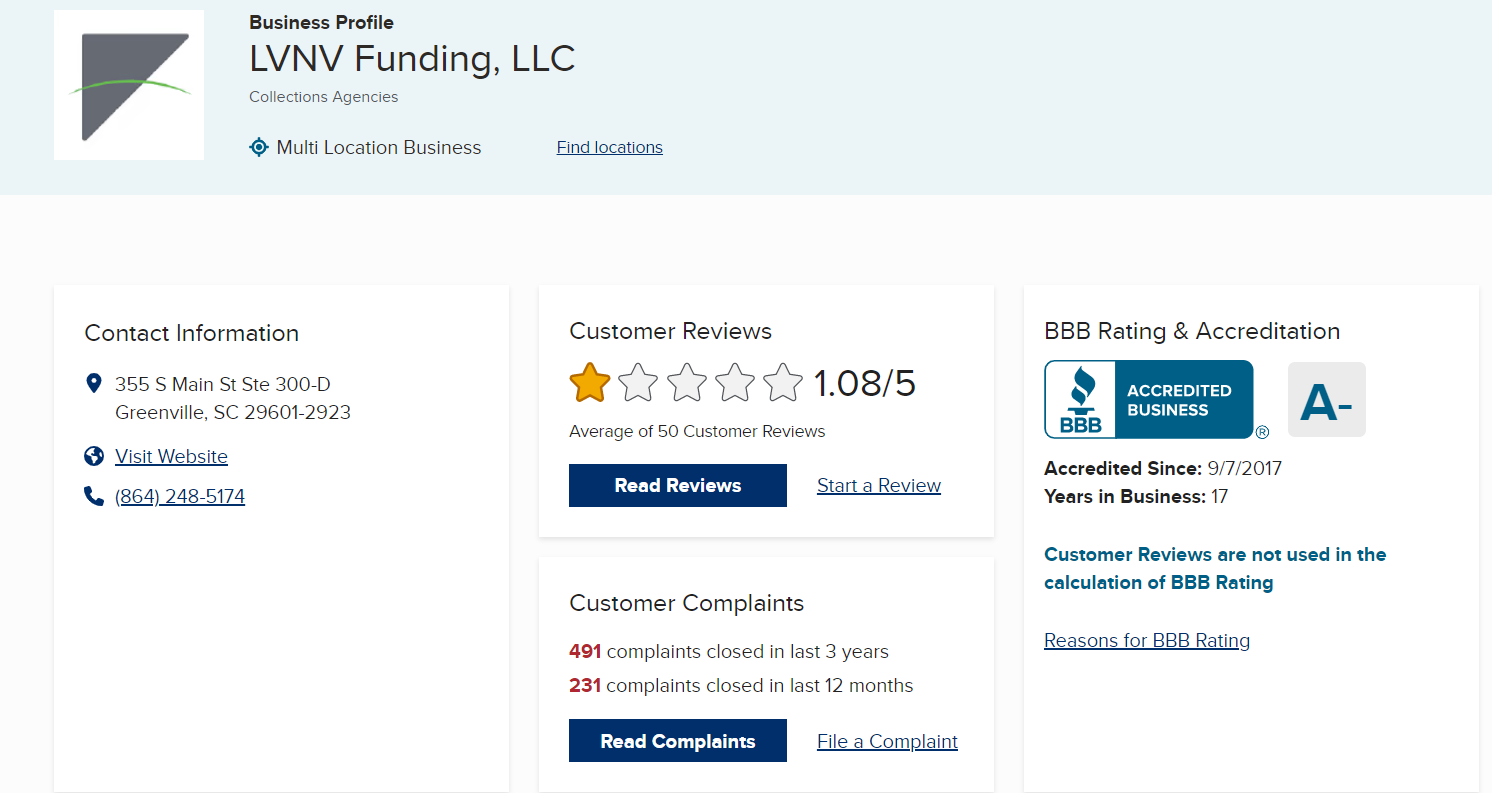

Contact Details

Phone numbers

Customer Service- (888) 665-0374, (864) 248-5174

Complaints- (866) 572-0262

Website: www.lvnvfunding.com

Mailing Address: LVNV Funding LLC, PO Box 10497, Greenville, SC 29603

Physical Address: LVNV Funding LLC, 55 Beattie Pl, Greenville, SC 29601

LVNV Funding History

After receiving a call or a lawsuit from LVNV Funding but not knowing about the company, you might wonder whether it is legitimate. LVNV Funding is a legitimate company in the debt collection business for more than 15 years. The company was accredited in 2017 by the Better Business Bureau. However, despite being a legitimately formed company, it is a subsidiary of related companies, and its corporate structure is a little confusing.

LVNV Funding LLC Reviews

Google Reviews

On Google, LVNV Funding has a 1.4 rating based on 34 Google reviews.

Let’s look at the BBB rating and reviews next.

BBB Rating, Reviews, and Complaints

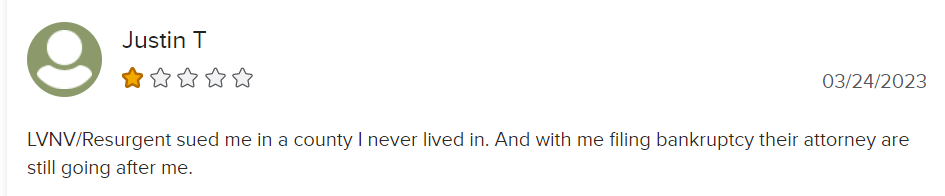

At the moment, there are 491 complaints on BBB made against LVNV Funding in the last three years, 231 of which BBB has successfully resolved over the past year. They have a pretty low rating of 1.08 out of possible five stars.

Customers reported some complaints. Here are the most recent:

Why is LVNV Funding on My Credit Report

Have you seen LVNV Funding on your credit report but do not remember obtaining debt from them? As we have discussed earlier, LVNV Funding LLC buys debt. Therefore, if they appear on your credit report, your original creditor charged off the debt, and LVNV Funding bought it.

How To Stop LVNV Funding LLC

You have received communication from LVNV Funding, and the calls or letters are getting out of hand. What do you do next? Here is how you stop LVNV Funding LLC

1. Use The 11 Word Phrase

You can end the call by saying, “Please cease and desist all calls and contact me immediately” Using this phrase should stop the debt collector from contacting you. If verbally using the phrase does not work, you can send a demand letter with the phrase.

According to FDCPA, once you ask a debt collector not to contact you, they should honor your request. The cease-and-desist letter should include your name, contact information, social security number, and address. It is important to send the letter through certified mail, preferably with a return receipt, to prove that the company received the letter.

Once the debt collector receives the letter, they should not contact you unless:

- They are writing back to you to acknowledge your request. On receiving the letter, they might send a reply acknew budging they received the letter and will not continue contacting you

- They are serving you. The debt collecting company can contact you to let you know they have filed a lawsuit against you.

2. Make LVNV Funding LLC Validate the Debt

After LVNV Funding reaches out to you, you should make them validate the debt. Although most people panic and rush to repay the supposed debt, verifying the debt is yours is important. Ask them to validate the letter. They should send a debt validation letter detailing the following:

- Your name

- Your creditor’s name

- How much you owe

- How to despite the debt

So, request a debt validation letter if you have not received one. If you have received the letter, or once you receive it, and the debt seems unfamiliar, request your credit report from either of the three agencies- Experian, TransUnion, or Equifax. The credit report will have all records of your credit history. See if the debt is genuine. If not, contact the credit bureaus and rectify the mistake.

How to Tell If It Is a Scam

Since LVNV Funding LLC is a large company, sometimes scammers impersonate an LVNV Funding agent. While it is not common, it sometimes happens. A legitimate agent of the company should have all your information. So, if the agent asks for personal information, it could be a scam. It is also likely to be a scam if the agent cannot give answers about the debt they are claiming you owe.

You can always ask for an employee ID number; if they cannot provide it, it is likely a scam. Always avoid giving out personal details to avoid being scammed. A debt validation letter is also a great way to avoid scammers.

Note: According to the new regulations, from November 30 2021, a debt collector should send a debtor a Notice of Debt within five days from the day they first contact you. So, if they call you today, they should send the Notice of Debt within five days. The notice should contain the following:

- The date of the last invoice or statement provided by the original creditor to the debtor

- Date of last payment the debtor made towards the date

- The date on which the transaction became a debt

- The charge-off date

- The judgment date in case there is a court judgment for the debt in question

These dates will help you establish if the statute of limitation applies to the debt. If the notice is incomplete or fails to include all the above, it is considered invalid, so the debt is not collectable.

It is important to know this because most debt collectors who bought debts before these new regulations do not have this information. Most of them can either get it from your original lender. However, to cut their losses, they might try to intimate you to repay the debt or get you to admit you are the debtor.

So, once the agency sends you a Notice of Debt, go through it to ensure it complies with the law. If it is not compliant with the law, write back to them, letting them know you will not engage in any further discussions until they send a Notice of Debt compliant with Regulation F

3. Confirm the Statute of Limitations on the Debt

If your debt is valid, check if it is still within the statute of limitations. Debts have a period after which a creditor or debt collector cannot file a lawsuit or take any measures to recover the debt. So, confirm the statute limitation on your debt, and see if the period has lapsed. If you are fortunate and the debt is time-barred, you might not have to pay it. Check the date of your debt against your state’s statute of limitation. Go through the statute of limitations by state to see your state’s limitations.

The statute of limitation is counted from the day the creditor reported the debt as delinquent. However, acknowledging the debt is yours or making a payment towards the debt will restart the statute of limitations. Failing to pay will keep the statute of limitation in place but will not remove the debt account from your credit history until seven years lapse. So, depending on your debt, the amount and your financial situation, if the statute of limitation is almost up, you might consider waiting it out.

4. Act

There are two actions you can take. You can pay up the debt or dispute it.

Paying the Debt

Once you ascertain the debt is yours, valid, and within the statute of limitations, settling your debt is the only way to keep LVNV Funding LLC at bay. First, you can choose to pay off if you have enough money. Consult LVNV Funding on where to make your payments when a debt is sold. It can be confusing knowing whom to repay.

Second, you can consider debt relief options like debt settlement. A debt settlement company can negotiate with the collecting company to allow them to accept a lump sum payment through less than the outstanding debt. Sometimes it works. Sometimes it doesn’t. However, you must be careful with debt settlement companies, as most are scams. A debt settlement company should not make any guarantees beforehand or charge fees before successfully setting your debt.

Third, you can consider credit counseling to get professional help managing your debt. You can also file for bankruptcy to get your debts forgiven. The best option for you will depend on your current financial situation.

Disputing the Debt

Sometimes the company may be reaching out about a debt that is not yours. In this case, you should dispute the debt. You have 30 days to dispute the debt after they contact you. After 30 days, the debt will be presumed valid, and you will be held liable.

When disputing the debt, send a debt validation letter following the template design for notices sent after the Regulation F implementation on November 20, 2021.

Does LVNV Funding LLC Sue for Unpaid Debt?

Yes. LVNV Funding is notorious for suing. Getting a debt collection company to file a lawsuit against you might be stressful and confusing. But there is a way to beat them.

Before discussing what to do and what not to do, it is important to note that LVNV Funding is mainly used as a last resort. Usually, they will make an initial phone call notifying you of a debt and asking you to settle it. Often, they offer a discounted one-payment alternative if you pay the debt within a specific date. They might call several times after that, especially if you do not make your payment. Sometimes, they might cross the line and harass you by contacting other people about your debt to get you to make your payment.

They will also report you to credit agencies (Experian, TransUnion, and Equifax). They will file a lawsuit against you if all their attempts are unsuccessful. Most debt collection agencies sue debtors hoping to get a default judgment against you. Most debtors do not know that most of these companies may be able to sue you, but they are ill-equipped. These agencies have an attorney who represents them in court. Often, these attorneys do not have enough knowledge or documentation on your case since they handle numerous suits. A common mistake debtors make is feeling intimidated after being sued, and without knowing what to do next, they fail to appear in court, and a default judgment is filed against them.

What You Can Do

If the LVNV Funding company has sued you, ensure you appear in court. It is best to hire an attorney if you can afford one. If not, you can research how to defend yourself. Either way, ensure you appear in court. Your appearance will show good faith and will not get the company a default judgment against you.

What You Can Avoid

Debt collection agencies like LVNV Funding get their way in court because their suits go uncontested. So, do not fail to appear in court. Failure to appear will see the court award full judgment to the debt collector. This can mean wage garnishment, frozen bank accounts, or other extreme but lawful measures against you. The court judgment may be listed in your credit report, affecting your ability to qualify for the credit and make the default public knowledge. So, do not fail to appear in court.

Understand Debt Collection

Receiving phone calls and letters from debt collection agencies all the time can be intimidating, and often, debtors panic and tend to ignore them. As much as you would like to ignore your debt collector, the issue will not disappear. You can, however, get as much information as you need on debt collection, what to do, and what not to do. Understanding debt collection will help you handle the issue calmly and with certainty. Do you have any questions on debt collection? Call or email us today.