Your voicemail box is full, but it’s not family and friends calling you to wish you a happy birthday, but it’s a debt collection agency such as Harris and Harris that are calling you every single day.

The tons of messages you get are beginning to give you anxiety issues, and you’ll like to stop them ASAP. This article will teach you how to stop Harris and Harris immediately.

What is Harris & Harris?

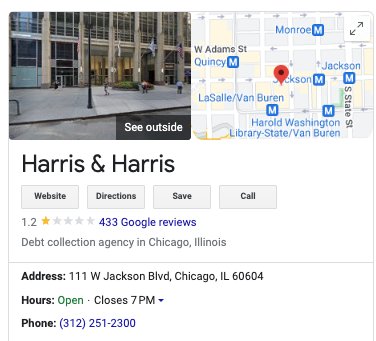

Harris & Harris Ltd is a popular debt collection agency in the United States.

The company has been collecting debts across many U.S. cities since it was founded in 1968. The organization has over 500 staff and is headquartered in Chicago, Illinois.

The company collects taxes, utilities, and government and healthcare debt.

Harris & Harris purchases your debts from a loan or credit card company and will contact you for payments. Upon refusal to make the requisite payment, Harris & Harris will call you regularly, leaving a negative rating on your credit report, or can also take action legally.

Other Names for Harris & Harris

The organization may pop up under one of these names in your credit report:

- Harris Collection,

- Harris Harris,

- Harris and Harris Debt Collectors,

- Harris and Harris Ltd,

- or Harris Ltd.

Contact Details

Pay A Debt: 1-800-362-0097

Phone Number: 1-866-781-4538

Email Address: moconnell@harriscollect.

Address: 111 W. Jackson Blvd, Suite 400 Chicago, IL 60604

Alleged FDCPA Violations

As stated by Washington’s attorney general, and also reported by Accounts Recovery. The alleged FDCPA (Fair Debt Collection Practices Act) violations of Harris & Harris, a collection agency, include:

- Making false and misleading representations. Harris & Harris allegedly made false and misleading statements to debtors, such as misrepresenting the amount of debt owed or threatening legal action that they had no intention of taking.

- Harassing or abusing debtors. The collection agency is accused of engaging in harassing or abusive conduct. For example, they called debtors repeatedly, used profanity or threatening language, and contacted third parties about the debt.

- Failing to provide certain disclosures. The amended lawsuit filed by the Washington State Attorney General alleges that Harris & Harris and other collection agencies failed to provide certain disclosures required by law. This includes the amount of the debt, the name of the creditor, and the debtor’s right to dispute the debt.

- Failing to verify debts. The collection agency is also accused of failing to verify debts when requested by consumers, as required by the FDCPA.

It is important to note that these are allegations at this point and the collection agency has not been found guilty of any wrongdoing.

Harris and Harris Reviews

Google reviews

Taking a glance at the reviews on Google suggests that albeit Harris & Harris is a legitimate company, consumers that have had experiences with them have a rather unpleasant one.

Of all 432 reviews on Google, it has an average of 1.2 stars. An abysmally low figure for a service provider.

Taking a closer look at the reviews suggests that of all 432 Google Reviews, only a few had a positive remark about the service.

The 5-star reviews hailed the company for a wonderful experience. A particular consumer hailed the company’s representative whose name is Deangelo. Consumers praised them for being helpful, patient, personable, and professional. They also commended the willingness of some staff to help resolve debt before it affects credit scores.

Among the see of 1-stars, many of them complained about the attitude of their staff. There are also incessant complaints about calls requesting that they make payment for debts that were settled. Further buttressing the complaints about them being scammers.

Verdict: Overall, reviews here suggest that although the company is legitimate. As such, you’ll need to regularly verify claims before making payment.

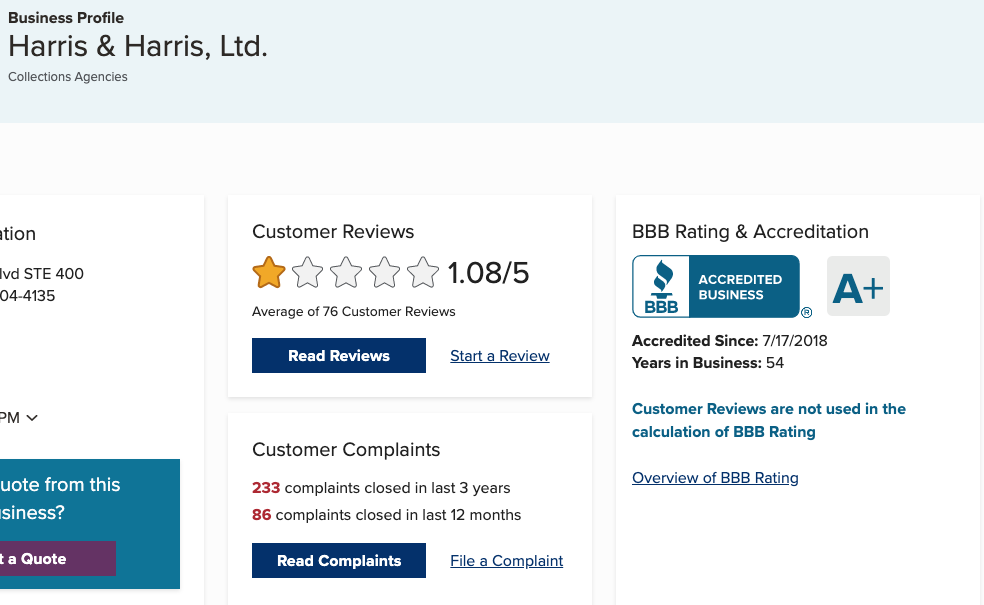

BBB reviews

As I surfed through the reviews on the BBB website for Harris & Harris Ltd, I noticed mixed experiences. Firstly, Harris & Harris has an average BBB rating of 1.08, one of the lowest in the market.

Some customers love the company’s efficiency, and willingness to cooperate with them. Some hail the company’s professionalism and advice. However, the bulk of reviews were complaints about the company’s lack of communication and tactics.

For example, a customer opined that he had a refreshing experience with Harris & Harris.

He further explained that the organization’s representatives were “helpful and courteous.”

Multiple reviews however say the company’s representatives were “rude and unprofessional.” They also felt that their concern wasn’t attended to. These divergent views are due to the individual experiences of users based on the representative that handled their case.

An interesting thing I noticed about the reviews is that some customers seemed to misunderstand the collections process itself. For example, one customer complained that the company was “harassing” them by calling them multiple times a day, even though this is a common practice in the collections industry. Other customers are unaware that collections agencies are legally allowed to contact their friends and family members to locate them.

How to Stop Harris & Harris

With these few simple steps, you can easily remove Harris & Harris from your credit report.

1. Use This 11-Word Phrase to Stop Calls

Are you getting incessant messages from debt collectors? Are you overwhelmed, such that you deliberately dodge calls from unknown numbers? Solving the problem is quite easy, as there’s an 11-word phrase that can make debt collectors stop calling you.

To take a much-needed break from incessant calls and harassment, you can make Harris stop by saying: “Please cease and desist all calls and contact with me, immediately.” Telling them that phrase will ensure that debt collectors stop contacting you via all available means.

2. Make Harris & Harris Validate the Debt

Per the regulations of the Fair Debt Collection Practices Act (FDCPA), collection agencies are required to validate your debt on request.

We recommend that you write a request for debt validation. If you’re being called for a debt you’re unsure of, then you should dispute it. As seen in reviews on Google and BBB, many customers claim that Harris calls them on debt they’re certain they’ve paid off. To prevent undue payment, you should request debt validation.

But even when you’re certain about the debt being requested, you should still request debt validation. It’s a great way to ascertain the exact amount you owe.

Also, Harris & Harris are third-party debt collectors, there’s a high probability that they lack the right document to validate your debt. If so, then request that they stop contacting you and remove their detail from your credit report immediately.

It’s best to act fast if you aim to validate your debt. Why? You only have 30 days after notification to send a debt validation letter. Here’s Harris & Harris’ form to dispute the debt – https://www.harriscollect.com/dispute/.

3. Confirm Debt is Within Statute of Limitations

The next step is to consider whether your debt is within the statute of limitation.

The statute of limitation is the timeframe for a debt collector to legally sue you and recover their timeframe varies from state to state Check here for the statute of limitation by state.

Here are some steps you can take to confirm if your debt is within the statute of limitations:

1. What type of Debt is it?

The statute of limitations differs from one debt to another. For example, medical debt, personal loans, credit card debt, and utility bills have different SOLs.

2. Identify the Statute of Limitation in your State

Use the link to check the laws in your state. You may also contact your state’s attorney general’s office or the consumer protection agency.

3. Determine the Start Date of the Statute of limitation

The statute of limitation starts from the date of the last payment on the account. If you’re not certain of the specific date, then request a copy. You can get your credit report from these three: TransUnion, Experian, or Equifax.

4. Check the Age of the Debt

You can calculate the age of the debt with your last payment. The creditor cannot legally sue for debt older than the SOL in your state.

4. Get legal advice

If you’re still not sure about your legal rights, then seek legal counsel. You can reach out to a lawyer with expertise in debt collection. They’ll help to understand your options and rights.

Note: Harris may still try to collect debts that are outside the statute of limitations. They may adopt an aggressive stance like phone calls and email harassment. However, they can sue if you know your rights.

5. Resolve the Debt

If it’s your debt, then resolve it.

Debt resolution is ideally a stressful and challenging process. However, there is a range of steps to managing it and ensuring you’re debt free. Here are some tips for resolving your debt:

1. Assess your debt. Gather all documents about the debt, such as credit card statements, loan agreements, and other related documents. Make a shortlist of your debts, including interest rates, minimum payments, and balances.

2. Create a budget. Make a budget that prioritizes your debt obligation. First, identify all necessary expenses like groceries, utilities, transportation, etc. Afterward, allocate the remaining funds towards your debt payments.

3. Discuss with creditors. Creditors would rather have collected lesser than the amount owed than opt for a court process. This is because litigations are both expensive and time-consuming.

As such, if you’re having trouble meeting up with payments, then contact your creditors and explain your predicament. They can offer you a temporary forbearance or deferment to help you get back on track.

4. Consider debt consolidation. You can consolidate multiple debts with a high-interest rate into a single loan with a lower interest rate. For this, explore options like personal loans, credit cards, or balance transfers.

5. Explore debt settlement. Debt settlement is for those that have a problem making debt payments in full. You may negotiate with your creditors to settle for an amount lesser than the full amount owed. However, this may negatively affect your credit score and should be considered an option of last resort.

6. Seek professional help: If you’re struggling to meet up with your debt payments, then seek help from a financial advisor or credit counseling agency. They can help create a budget, develop a debt repayment plan, and manage your debt.

Having in mind that debt resolution takes time, and requires discipline and patience. By having a solid commitment and plan, you’ll eventually settle your debt and become free.

Harris and Harris Alternatives

Let’s consider a few alternatives to Harris.

Debt Management

Debt Management is also called credit counseling. In this alternative, the company negotiates the interest on your credit card debt.

Debt management companies are usually non-profit organizations that charge between $30-$50 as their monthly fee. This may not negatively impact your credit score, and the duration usually ranges from 3-5 years.

Haven said that debt settlement vs debt management may not save you much money. Thus, you may opt for another option–bankruptcy.

Bankruptcy

Filing bankruptcy may be an option of last resort for multiple reasons. A Chapter 7 bankruptcy for example will remain on your credit report for 10 years. Chapter 13 bankruptcy will remain on your credit report for 7 years. For example, Chapter 13 will provide debt relief, and immediately stop Harris & Harris from contacting you for 3-5 years. Chapter 7, it’ll forgive all your debt for 120 days, pending the determination of your case.

Haven said that Chapter 7 bankruptcy remains the cheapest and quickest debt relief option to get. You can check if you qualify for Chapter 7 bankruptcy debt relief using a Chapter 7 means test calculator.

Conclusion

Harris is a debt collection agency that purchases bad loans from creditors and recovers the debt. Harris & Harris’s reviews show that the company is legitimate, albeit with multiple complaints about its service.

Before opting for their service, you might want to first research the Consumer Finance Protection Bureau’s guidance on lawsuits and debt settlement.