Are you afraid of picking up your phone or listening to your voicemail messages because the CBE Group has been calling you endlessly? Even if you are falling behind on debt, you still have options. If the CBE group has been on your neck for an outstanding debt, here is what you can do to stop them.

Should you pay a debt collection agency?

Let’s look at who CBE Group is and how you can deal with them.

Background on the CBE Group

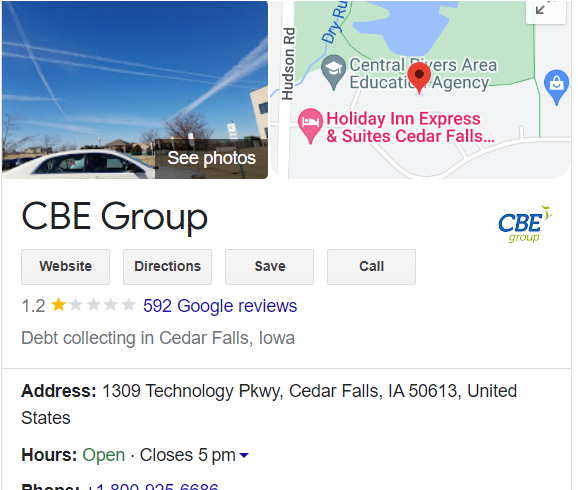

It is a debt collection agency that has been in the debt collection industry since 1933. It appears a legitimate agency accredited by the Better Business Bureau, meaning it meets specific accreditation standards. CBE Group Collects different types of debts, including student loan debts, bank cards, telecommunications, and healthcare debts. Their headquarters are in Cedar Falls, but they also have call centers in Tennessee, Texas, and the Philippines. CBE Group’s phone number is 1-800-925-6686

The CBE group is among the few agencies with a contract to collect student loans on behalf of the United States Department of Education and overdue federal taxes for the IRS. The CBE group has a reputation as a large debt collection agency.

Despite the impressive BBB rating, customers have complained about intimidation tactics used to coax them into making payments. CBE group has been reported to harass and bully customers by making dozens of calls daily, calling others by mistake, and failing to acknowledge cleared debts. Are you a victim of the same? We can help you stop CBE Group today.

Is CBE Group Legitimate?

With the numerous complaints and aggressive measures by the CBE group, most people wonder if the CBE Group is legitimate. The CBE group is legitimate, as verified by the Better Business Bureau certification. The company was founded decades ago, in 1933, incorporated in 1985, and was accredited by the BBB in 1992.

Note: Take note of fake companies in the industry purporting to be CBE Group. If the company contacts you, the first step is to validate the company.

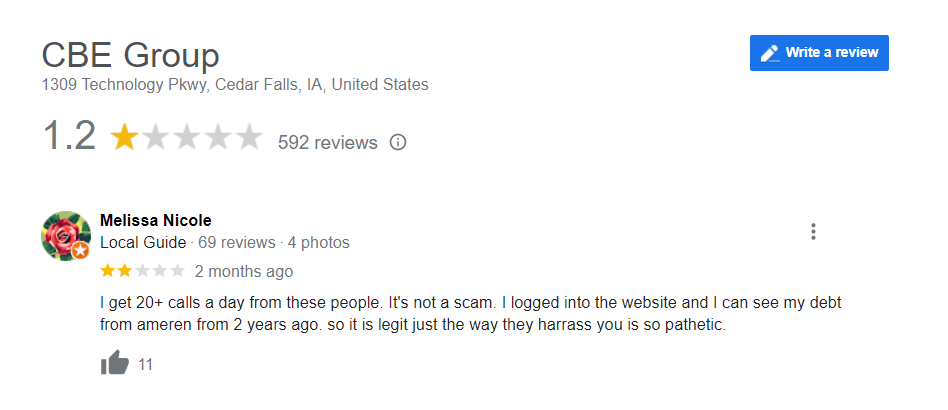

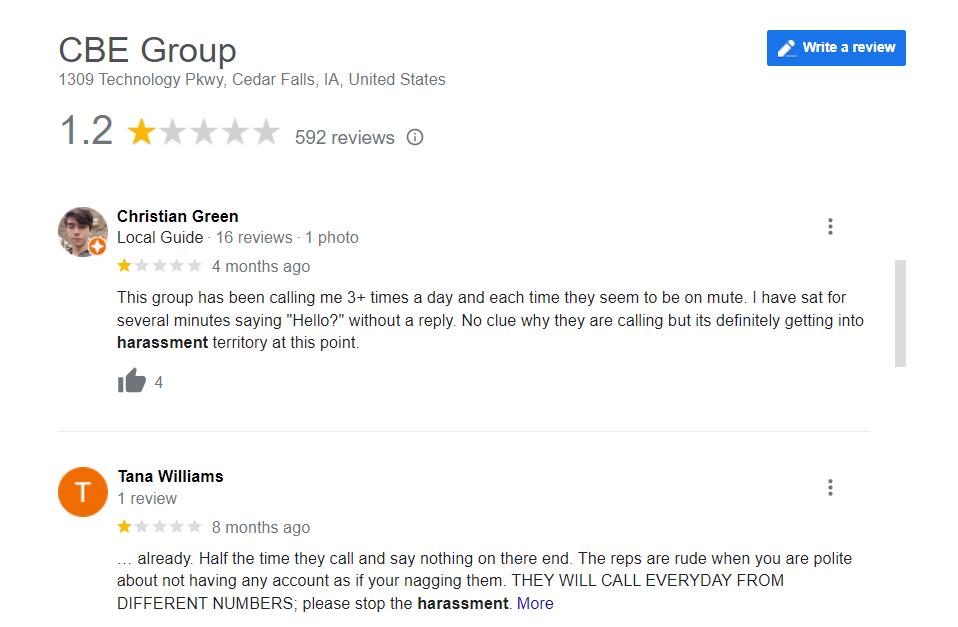

Google Reviews

Currently, the CBE Group has 592 reviews and a 1.2-star rating. There are numerous complaints from customers

The low rating is from the numerous customer complaints, most of which point out harassment by the CBE Group.

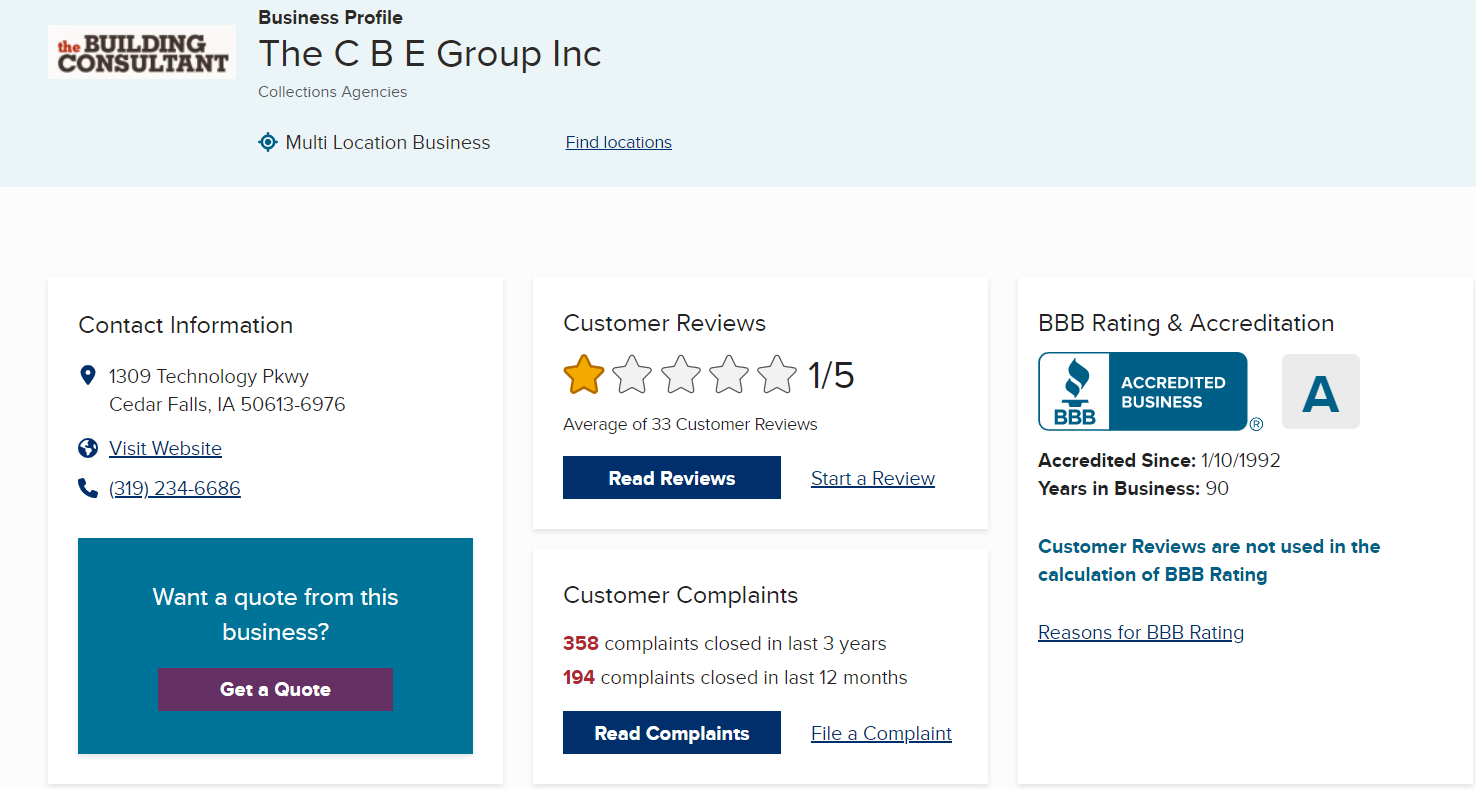

BBB Reviews and Complaints

The BBB has, to date, closed 358 complaints in the last three years against the CBE Group and 194 complaints in the last year. Most of these complaints have been about the company’s unprofessionalism regarding class, and others say they were contacted about debts the company could not validate.

How To Stop CBE Group

Here is a step-by-step process on how you can stop the CBE Group.

1. Use an 11 Word Phrase to Stop the Calls

Are you tired of the endless calls from the CBE Group? There is an 11-word phrase you can use to stop these calls.

The phrase: “Please cease and desist all calls and contact me immediately.”

You can use these eleven magic words to keep debt collectors, including the CBE Group, at bay. While you may have failed to repay your debt on time, you still have rights as a debtor. You can use the phrase to stop a debt collection agency from phoning you.

2. Make CBE Group Validate the Debt

Man is to err, and sometimes, the CBE group might contact you erroneously. So, once the CBE group agent reaches out to you, and you verify the company, next, validate your debt. If you are unsure of the debt they are contacting you about, seek clarification by sending a Debt Validation Letter. Check your credit report here and see if the debt is on your credit report.

3. Confirm Debt Is Within Statute of Limitations

Did you know that there is a statute of limitations on debts? The statute of limitations is a predetermined period during which a creditor or debt collector has to sue a debtor to revolver their debt. If the period lapses, then the creditor or debt collection agency cannot take any measures to recover the debt.

Most debts have a limitation period of six years from your last payment or after you wrote to them. The period, however, differs depending on debts. For example, mortgages have a longer time limit. For example, if you have fallen behind on your mortgage payment for a few months, your lender repossesses your home. However, you still owe them. They have six years to recover the interest on the loan and 12 years to recover the principal amount. Here is information on the statute of limitations by state.

Your debt can be statute barred if your lender takes too long to take measures to recover the debt. However, this does not mean your debt is written off. Your debt continues to exist, but your lender cannot take legal action, e.g., file a lawsuit to recover the debt. Therefore, waiting until your debt is statute-barred does not mean it ceases to exist.

A debt is statute-barred if the debt holder(s) have not made any repayment towards the outstanding debt, the debtor(s) and their representation have not acknowledged the debt, and if the creditor did not take legal action to recover the debt.

When did you last make your payment? Check the date, calculate, and see if your debt is statute-barred or within the limit. If the debt is within the limit, ensure you collect the information on the debt and start working out a repayment plan. If not, you can use it against your lender in court.

4. Resolve the Debt

Once you confirm the debt is within the statute, it is time to resolve it. There are two ways to do this. First, confirm if the debt is yours or not. If it is, then you should work on settling it. If not, dispute it.

Settling the Debt

After the CBE Group contacts you, and you acknowledge you are the debt holder and the debt is within the statute of limitations, you can work on settling it. You can discuss the debt with the Group and see if they will be willing to settle for less than the original cost of the debt. If they are not open to settling, you can discuss a payment plan for the debt.

Most debt collectors are open to setting up a plan to recover the debt. Should they agree to work out a payment plan, or a settlement, have the agreement in writing. Write the newly negotiated amount and the payment terms before making any payments.

If you have money to pay off the debt, pay it off. If you have been paying the debt timely, you can ask the CBE Group for goodwill deletion. Write a clear letter with your request, explaining why you need the goodwill deletion. Include how the debt was transferred to the debt collections agency and how you intend to correct the issue. They will determine whether to remove the item or not.

The CBE Group can refuse to delete. If they accept to delete the debt, they are not obliged to delete the information from your credit report. Nevertheless, paying off your debt is beneficial even if the record remains on your credit report; it may not affect your credit score.

Disputing the debt

If the CBE group contacts you about a debt you believe is not yours, you can dispute it. You should write a dispute letter and send it to the agency within 30 days of them contacting you. Send the letter to the credit reporting agencies and have them investigate the debt. If they cannot verify the debt, it will be deleted from your credit report.

All debtors have a right to dispute a debt as stipulated in the Fair Credit Reporting Act (FCRA) in Section 609. Thus, credit dispute letters are often known as 609 letters. After 30 days, the collector will be required to cease any efforts to collect the debt, including communication, until they verify the debt and prove you are the valid debt holder.

Pro Tip: Ensure you have a date on the dispute letter and have a copy to prove you sent it. For example, if you have sent your letter through the mail, ensure you keep a copy. Note that you can only dispute if the debt is inaccurate.

What Should I Write in My Dispute Letter

The letter should contain the following:

- Your full name

- Contact information

- The name and contact of the CBE Group

- Request asking them to communicate how much you owe on the alleged debt

- A request asking the agency for the name of the original creditor and their contact information

- A request to show proof of the debt

Work with a Lawyer to Write a Dispute Letter

Having to deal with a debt collection agency for a debt you know nothing about can be overwhelming. We recommend working alongside a lawyer if you can draft a dispute letter. The lawyer knows what to write and leave out the letter. Besides, they can ensure the filing deadline is within the time limit set by the FDCPA. A lawyer can easily identify false statements made by the collection agency, threats, or other malpractices by the debt collection agency, which they can use in your defense.

Know your rights

Most debtors think there isn’t much they can do because they are falling behind on debt and are in the wrong after ignoring the debt collector. Despite your delayed loan repayment, you have your rights as a debtor. No debt collector, including the CBE Group, should:

- Reach out to any other person, e.g., your family, or contacts, in an attempt to communicate with you. They can only communicate with you through your attorney or a consumer reporting agency.

- Call earlier than 8:00 am or later than 9:00 pm

- Use any misleading or false information regarding the debt

- Add extra charges fees, interest, or any additional charges on the original outstanding debt]

- Use abusive language, or harass you about the debt

- Call your employer or your workplace if your employer prohibits you from such communication at the workplace

Take Legal Action Against CBE Group

You can choose to take legal action to stop the CBE Group if the above methods and the 11-word phrase do not work. It is best to work with an experienced debt collection lawyer to discuss your options. However, you have a strong case if:

- You have been receiving calls early in the morning before 8 am or later in the evening after 9 pm from the CBE Group and can prove it

- They are using obscene language to try and coax you into paying

- The agency is making criminal accusations against you or is attempting to intimidate you by threatening you with arrest, violence, lawsuits, or a negative credit report.

- They are contacting others about your debts,

- You are receiving calls at work, and or if the calls are automated robocalls.

A debt collection attorney will review your case and advise accordingly.

Does CBE Group Sue for Unpaid Debt?

Yes, the CBE Group sues debtors over unpaid debt. However, they do not always sue. It will depend on your willingness to cooperate and repay the debt or work out a repayment plan.

Will CBE Group sue or garnish your wages?

As a debt collection agency, the CBE group can take various measures to collect debt. They can reach out to you constantly or take legal measures, like suing you and garnishing your wages. Therefore, if their efforts to reach out to you are unsuccessful, they can file a lawsuit against you requesting to garnish your wages. If the court approves their request, then your wages might be garnished.

The laws on wage garnishment vary from state to state. Go through the wage garnishment laws in your state to understand your options. As a legal debt collection agency, the CBE group has the right to contact you and follow up on an outstanding debt. However, under the Fair Debt Collection Practices Act, FDCPA, the Group, and other debt collection agencies should stop contacting you if you ask them to. This will likely force them to take legal action against you, usually a lawsuit.

If the CBE Group has sued you for a debt you are not responsible for, it is important to consult an attorney familiar with debt collection cases.

How Debt Collection Answers Can Help

Nobody wants to deal with numerous calls and never ending letters from the CBE Group, especially when the debt information is inaccurate. Unfortunately, debt collection agencies often make mistakes, and identity theft doesn’t make it any better. Understanding how debt collection works is important. You will know what to do once you get a call from debt collecting agencies. It will also help you know how to keep debt collectors at bay. You will also understand your rights should you find yourself in this situation. Have any debt collection questions? Contact us for free today!

Contact Information

Main Mailing Address:1309 Technology Pkwy, Cedar Falls, IA 50613

Other Mailing Addresses: 607 S. Business, I-35 # 105, New Braunfels, TX 78130, 326 Innovation Way, Clarksville, TN 37042

Website:www.cbegroup.com or https://www.cbecompanies.com/