Did you receive a letter from 1 American lane suite 220? Are you wondering what the Cavalry SPV I, LLC agency is? Should you pay this collection agency? You may feel uncertain once you receive a notice that they are petitioning you, and you might even think that the legal action is a fraudulent scheme and disregard it.

Also known as Cavalry Portfolio Services, LLC, and Cavalry, this debt collection agency acquires and manages non-performing consumer loan portfolios. You may be unfamiliar with Cavalry SPV I because this agency is neither a creditor nor a lender. The following paragraphs provide information about Cavalry SPV I, LLC, and suggest possible actions you may take if you find yourself facing a lawsuit from them.

What is Cavalry SPV I LLC?

Cavalry SPV I, LLC is a leading company specializing in managing and acquiring nonfeasance end-user loan portfolios. Its primary goal is to assist people in resolving their debt by providing affordable solutions while ensuring a professional experience.

Creditors often sell old debts, such as credit card debt and personal loans, that they have been unable to collect or do not anticipate to collect to agencies like Cavalry SPV I, LLC at a snippet of the arrears. Once the debt buyers acquire the credit, they seek the total credit from the debt holders, often using disputation to track the debt. Receiving threats of a suit from Cavalry Portfolio Services means that this company purchased an outstanding debt from your lender.

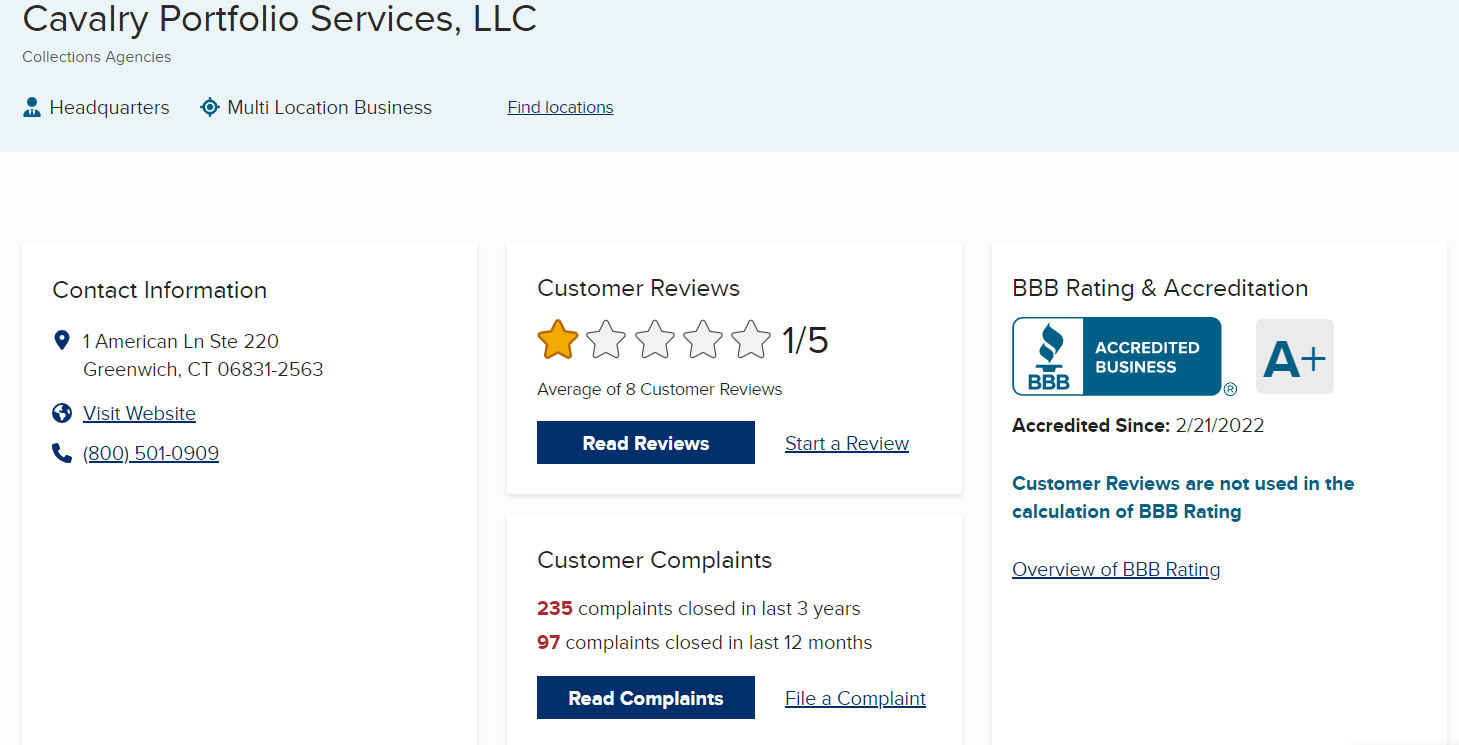

Contact Details

As one of the largest debt buyers in the nation, you can contact Cavalry SPV I, LLC directly at 866-483-5139.

Alternatively, you can visit Cavalry to discuss your options at the below address:

1 American Lane

Suite 220

Greenwich, CT 06831-2200

Or through their website: https://www.cavalryportfolioservices.com/contact

Cavalry SPV I, LLC History

Cavalry SPV I, LLC is a private limited liability company based in New York. The company was founded in 2002 and is a Cavalry Portfolio Services, LLC subsidiary headquartered in Valhalla, New York.

For example, Cavalry SPV I, LLC operates as a Special Purpose Vehicle (SPV) that purchases debt portfolios from creditors and repackages them for sale to other investors.

Cavalry SPV I, LLC Reviews

Cavalry SPV I, LLC has been specializing in securitization and asset management services for a long time. In some cases, individuals who owe debt may feel harassed or mistreated by Cavalry SPV I, LLC, leading to negative reviews of the company’s practices.

Some of the malpractices may include:

- Using deceptive and misleading statements

- Contacting individuals at inconvenient times

- Engaging in threatening tactics.

Reviews

Based on the customers’ complaints provided, Cavalry SPV I, LLC is aggressive in its collection tactics and may not follow ethical practices.

Regarding debt, it’s essential to take action to avoid receiving a summons and complaint from Cavalry SPV I, LLC. Receiving a summons and complaint means legal action has been taken against you, and you will have 20 days to respond to the lawsuit.

If you receive a default judgment, Cavalry SPV I, LLC may have the right to garnish your wages. This can negatively impact your credit report, making it challenging to apply for loans in the future.

Ultimately, how you handle debt collection from Cavalry SPV I, LLC depends on your situation. If the debt is relatively small, paying it off may be best to avoid affecting your credit report. You can also negotiate a settlement with them, often for much less than they claim you owe.

BBB Reviews

The company has an A+ rating from BBB, and 235 complaints in the past three years, with only 97 complaints resolved in the past year.

Other Reviews

Other complaints suggest that Cavalry SPV I, LLC may engage in predatory collection practices by resubmitting old debts and attempting to take individuals to court over relatively small amounts. Here are recent reviews by customers:

The company may need to be more responsive to customers’ complaints and may not be willing to work with individuals to resolve their debts.

How To Stop Cavalry SPV I LLC and Resolve the Debt

Do you find yourself overwhelmed and frustrated by the persistent calls from the Cavalry SPV I LLC? If so, you’re not alone. Luckily, there are steps you can take to put an end to their relentless attempts to contact you.

Step 1: Utilize an Effective Phrase to Halt the Calls

Are you tired of constantly receiving calls from the Cavalry SPV I LLC, interrupting your daily routine and causing you stress? Fortunately, there is an effective way to stop these calls in their tracks. By using an eleven-word phrase, you can put an end to the Cavalry SPV I LLC constant calls.

The phrase that you need to know is, “Please cease and desist all calls and contact me immediately.” By uttering these powerful words, you can keep debt collectors like the Cavalry SPV I LLC at bay, while also exercising your rights as a debtor. It’s a simple but effective solution to an issue that can otherwise feel overwhelming.

Step 2: Ensure the Validity of the Debt

Mistakes can happen, and sometimes the Cavalry SPV I LLC may contact you regarding a debt that you don’t even owe. To avoid any confusion or further harassment, it’s important to ensure the validity of the debt before proceeding with any payments.

When the Cavalry SPV I LLC contacts you, first verify that the company is legitimate. Then, take the necessary steps to validate your debt. If you’re unsure about the specifics of the debt, consider sending a Debt Validation Letter. Additionally, check your credit report to see if the debt is listed there.

Step 3: Know the Limitations Period for Your Debts

The statute of limitations is a predetermined period within which a creditor or debt collector has to sue a debtor to recover their debt. Most debts have a limitation period of six years from the last payment or acknowledgement. However, the period may vary depending on the type of debt.

For instance, mortgages have a longer time limit. If you fall behind on your mortgage payments, your lender can repossess your home, but you still owe them. They have six years to recover the interest on the loan and 12 years to recover the principal amount. It’s important to know the specifics of the limitations period for your debts to avoid being taken advantage of by debt collectors.

Determine Whether Your Debt is Statute-Barred

If your lender or debt collector takes too long to take measures to recover your debt, your debt may become statute-barred. This means that your lender cannot take legal action, such as filing a lawsuit, to recover the debt. However, this does not mean that your debt ceases to exist.

A debt is considered statute-barred if the debt holder(s) have not made any repayment towards the outstanding debt, the debtor(s) and their representation have not acknowledged the debt, and the creditor did not take legal action to recover the debt. To determine whether your debt is statute-barred, check the date of your last payment and calculate if it’s within the limitations period.

Collect Information and Take Action

If your debt is within the limitations period, it’s important to collect all the necessary information on the debt and start working out a repayment plan. On the other hand, if the debt is statute-barred, you can use this as a defense against your lender in court.

Understanding the statute of limitations for your debts can help you protect your rights as a debtor and prevent undue harassment from debt collectors. Make sure you know your rights and take action to protect yourself..

Step 4. Resolving the Debt

When it comes to resolving the debt, you have two main options: settling the debt or disputing it. If the debt is yours, you should work on settling it. If not, you should dispute it.

Settling the Debt

If the debt is yours and is within the statute of limitations, you can work on settling it. The first step is to discuss the debt with the collection agency and see if they are willing to settle for less than the original cost of the debt. If they are not open to settling, you can discuss a payment plan for the debt.

Most debt collectors are open to setting up a payment plan to recover the debt. If they agree to work out a payment plan or a settlement, make sure to have the agreement in writing. Write down the newly negotiated amount and the payment terms before making any payments.

Goodwill Deletion

If you have been paying the debt timely or have the money to pay it off, you can ask the collection agency for goodwill deletion. Write a clear letter with your request, explaining why you need the goodwill deletion. Include how the debt was transferred to the debt collections agency and how you intend to correct the issue.

It’s important to note that the collection agency may refuse to delete the debt. If they do agree to delete the debt, they are not obliged to remove the information from your credit report. However, paying off your debt is beneficial even if the record remains on your credit report, as it may not affect your credit score.

Disputing the Debt

To dispute a debt, you should write a dispute letter and send it to the agency within 30 days of their initial contact. It’s important to note that under the Fair Credit Reporting Act (FCRA) in Section 609, all debtors have the right to dispute a debt. These letters are often referred to as 609 letters.

When you send your dispute letter, make sure to include a date and keep a copy of the letter for your records. If you send the letter through the mail, ensure that you keep a copy of the tracking number as well.

Once the agency receives your dispute letter, they are required to investigate the debt within 30 days. If they cannot verify the debt’s validity, it must be deleted from your credit report.

It’s important to note that you can only dispute a debt if it is inaccurate. If the debt is yours, but you are disputing the amount owed, this may not be grounds for a dispute. However, if the agency cannot verify the debt’s accuracy, they must stop all attempts to collect the debt until they can prove that you are the valid debt holder.

If you believe that a debt collection agency is attempting to collect on a debt that is not yours, it’s important to take action and dispute the claim. One of the most effective ways to do this is by writing a dispute letter to the agency. However, it’s important to ensure that your letter contains all the necessary information and is written in a way that is clear and concise.

What to Include in Your Dispute Letter

Your dispute letter should include the following information:

- Your full name and contact information

- The name and contact information of the debt collection agency

- A request for the agency to communicate how much you owe on the alleged debt

- A request for the name of the original creditor and their contact information

- A request for the agency to show proof of the debt

Working with a Lawyer to Write a Dispute Letter

Dealing with a debt collection agency can be overwhelming, especially if you know nothing about the alleged debt. We recommend working alongside a lawyer to draft a dispute letter. A lawyer can ensure that the letter is written in a way that is clear and concise, while also ensuring that all necessary information is included.

Additionally, a lawyer can ensure that the filing deadline is within the time limit set by the FDCPA. They can also identify any false statements made by the collection agency, threats, or other malpractices, which they can use in your defense.

What Debt Collectors Cannot Do

Debt collectors are not allowed to engage in certain behaviors when attempting to collect a debt. These include:

- Contacting any other person, such as your family or contacts, in an attempt to communicate with you. They can only communicate with you through your attorney or a consumer reporting agency.

- Calling earlier than 8:00 am or later than 9:00 pm.

- Using any misleading or false information regarding the debt.

- Adding extra charges, fees, interest, or any additional charges on the original outstanding debt.

- Using abusive language or harassing you about the debt.

- Calling your employer or your workplace if your employer prohibits such communication at the workplace.

It’s important to note that these guidelines are in place to protect you from harassment and abuse by debt collectors. If a debt collector violates any of these guidelines, you have the right to take legal action against them.

Understand Your Rights

You may have a strong case against the Cavalry SPV I LLC if they have engaged in any of the following behaviors:

- Contact you early in the morning before 8 am or later in the evening after 9 pm, and you can prove it.

- Using obscene language or making threats to coerce you into paying the debt.

- Making criminal accusations against you or attempting to intimidate you by threatening you with arrest, violence, lawsuits, or a negative credit report.

- Contacting others about your debts.

- Contacting you at work or using automated robocalls.

If you have experienced any of the above behaviors, it’s important to take action to protect your rights as a debtor.

Working with a Debt Collection Attorney

If you believe that you have a strong case against the Cavalry SPV I LLC, it’s important to work with an experienced debt collection attorney. They can review your case and advise you on the best course of action to take. They can also represent you in court if necessary, helping you to seek the compensation you deserve.

Understanding Cavalry SPV I LLC’s Approach to Unpaid Debt

While the Cavalry SPV I LLC may ultimately pursue legal action against you, it’s important to note that they are required to follow certain guidelines when doing so. For example, they cannot make false or misleading statements about the debt, and they cannot threaten you with legal action unless they actually intend to follow through.

If you’re concerned about the possibility of being sued by the Cavalry SPV I LLC or any other debt collection agency, it’s important to work with an experienced debt collection attorney. They can help you understand your rights and options, and can represent you in court if necessary.

Understanding Cavalry SPV I LLC’s Actions in Debt Collection: Can They Sue or Garnish Your Wages?

If the Cavalry SPV I LLC files a lawsuit against you and the court approves their request to garnish your wages, a portion of your wages may be taken to pay off the outstanding debt. It’s important to note that the laws on wage garnishment vary from state to state, so it’s important to research the specific laws in your state to understand your options.

While the Cavalry SPV I LLC has the right to contact you and follow up on an outstanding debt, they are also required to follow certain guidelines.. If you ask them to stop contacting you, they are legally required to do so. However, if they are unable to reach you through other means, they may choose to take legal action against you.

If you believe that the Cavalry SPV I LLC has sued you for a debt that you are not responsible for, it’s important to consult with an attorney who is familiar with debt collection cases. They can help you understand your rights and options and represent you in court if necessary.

Get Your Debt Collection Questions Answered with Debt Collection Answers

At Debt Collection Answers, we offer free resources and information to help you understand debt collection and your rights as a debtor. Whether you have questions about debt validation, debt settlement, or debt collection lawsuits, we can help you find the answers you need.

Our experienced team of debt collection experts can provide you with the knowledge and tools you need to navigate the complex world of debt collection. We can help you understand your rights under FDCPA and other relevant laws, and can provide you with practical advice on how to deal with debt collection agencies.

Conclusion

If you’re dealing with debt collection agencies like the Cavalry SPV I LLC, it’s important to understand your rights and options. By getting your debt collection questions answered with Debt Collection Answers, you can gain the knowledge and confidence you need to take control of your debt and protect your financial future. Contact us for free today and let us help you get started. Remember, writing with a high degree of perplexity and burstiness can help you convey complex ideas effectively and ensure that your message is communicated clearly and concisely.